The French Organic Market 2017 is taken from Agence Bio 2017 report. The link to download the entire French Organic Market Report 2017 , in French naturally, is at the bottom of this article.

French organic market continues it’s rapid Growth

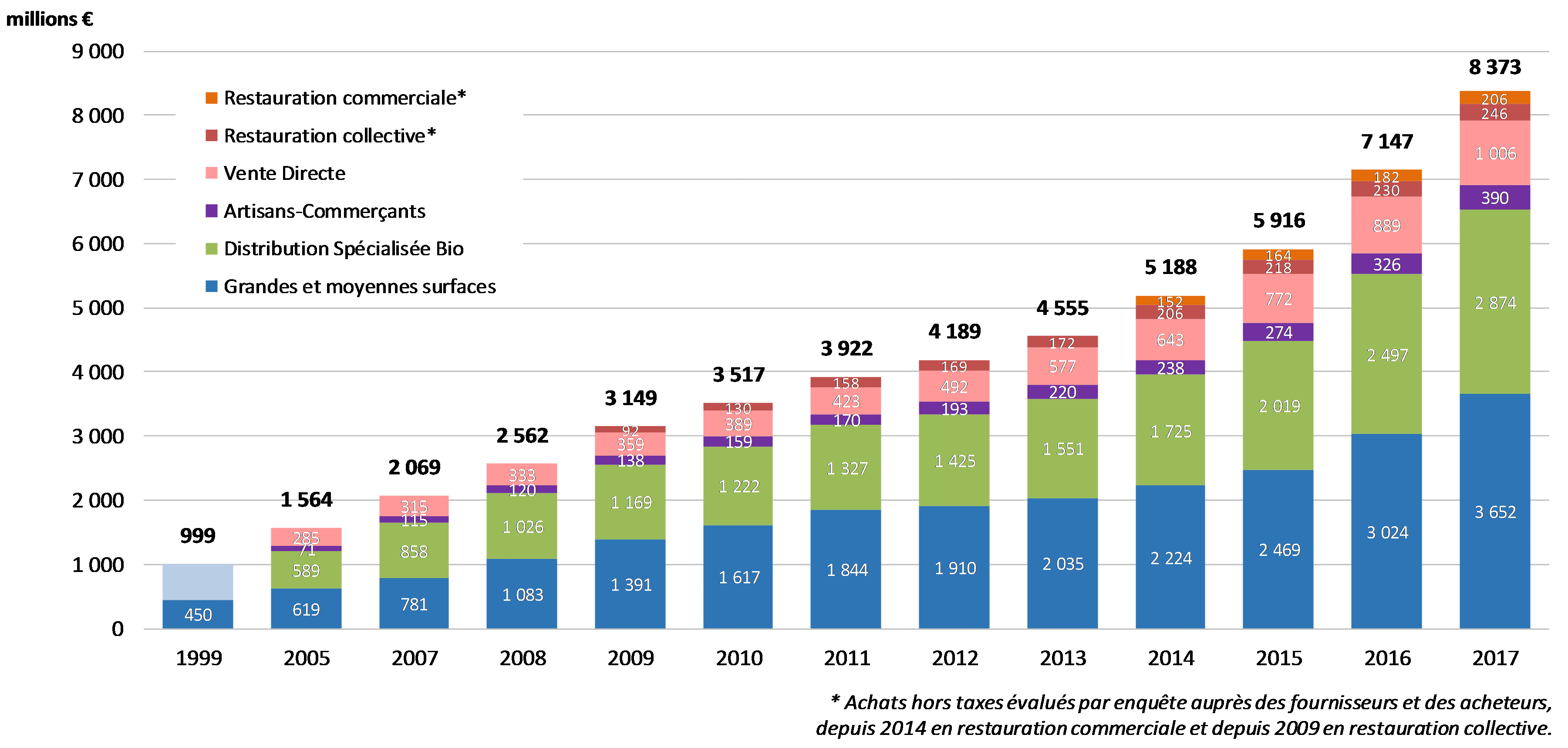

In 2017, the value of purchases of food products from organic farming is estimated at 8.373 billion euros, a growth of nearly 17% vs 2016, results higher than the Agence Bio estimates of last February.

- € 7.921 billion including household consumption at home

(+ 18% versus 2016), which represents 4.4% of general consumption

of food products - € 452 million excluding purchases of organic products served in restaurants, out of home including € 246 million excluding tax in catering (+ 7% in 2016) and € 206 million excluding tax in commercial catering (+ 13% since 2016).

Evolution of organic turnover by distribution channel from 1999 to 2017

Source: BIO Agency / AND-i 2018

To find out more about organic foods in collective catering

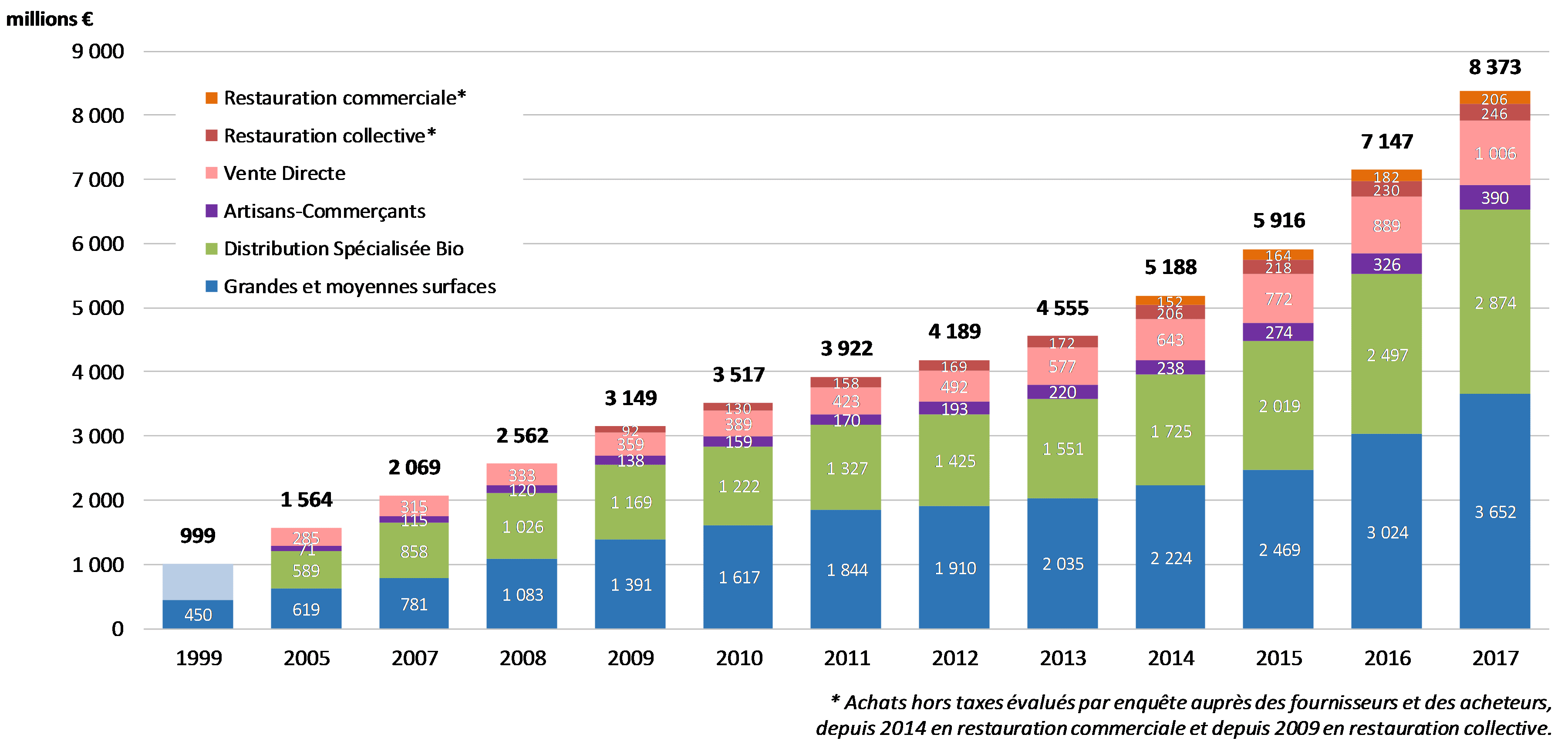

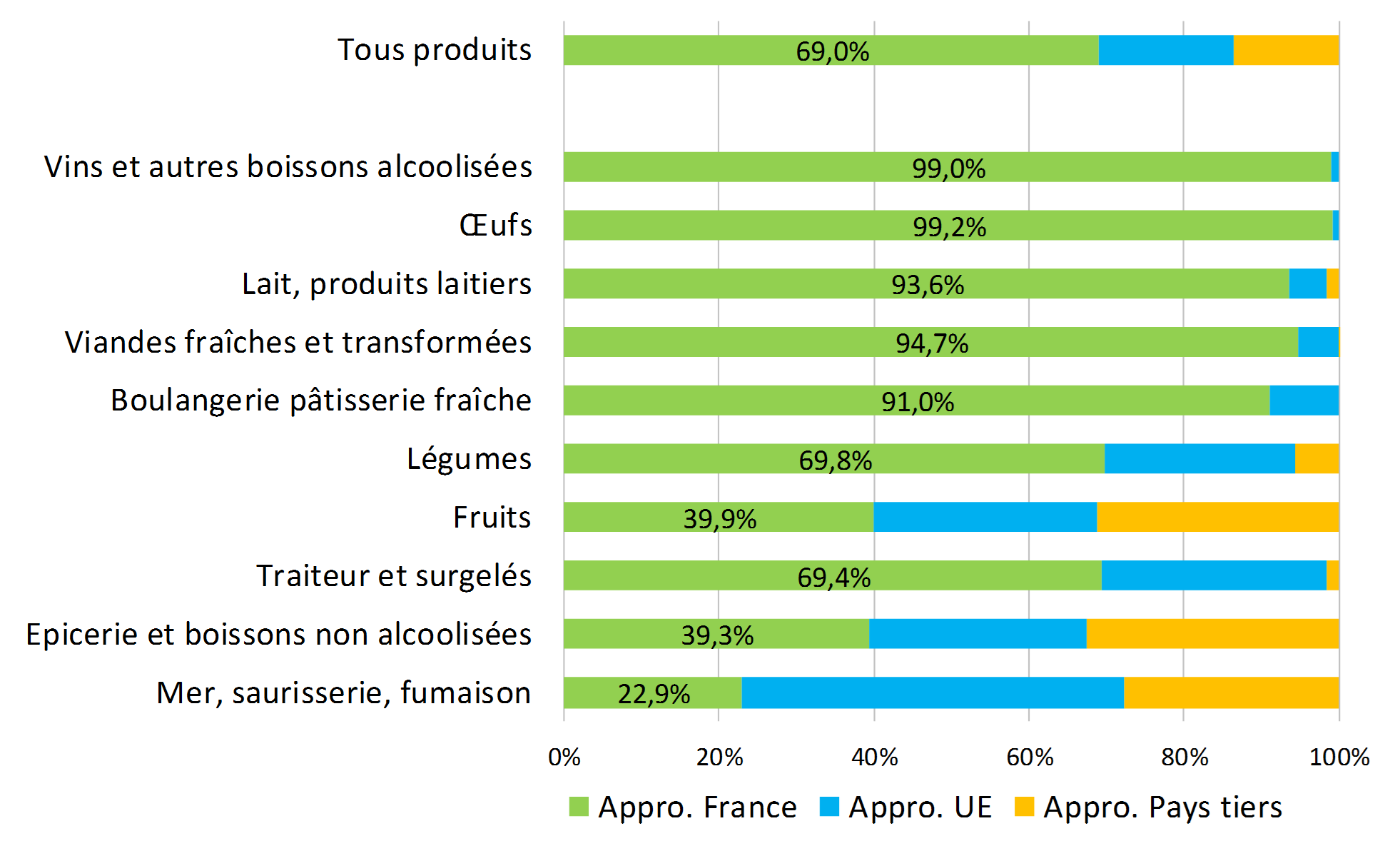

French Organic Market according to product category

In the French organic food market, in structural terms, more than half of sales in value of organic products are made in the fresh food category.

In 2017, as in 2016, the main contributors are groceries (31% of growth), fresh fruits and vegetables (17%) and alcoholic beverages (15%).

A new trend is emerging: processed products are the most dynamic with caterers (+ 34%), drinks: fruit juice (+ 23%), ciders, beers (+ 26%) and wines (+ 21%).

As in 2016, the dry-food category is particularly dynamic with + 22% in salted groceries and + 17% in sweet groceries. A success due in particular to aperitif products, infant foods, oils, as well as more specifically in supermarkets, with the sweet section with breakfast products and canned fruits.

Fresh fruit and vegetable sales continued to grow by 16% vs. 2016, reflecting the development of the volume consumption of all products, notably bananas and citrus fruits, with a relatively low average price evolution (+ 2%).

Distribution of household purchases for home consumption of organic products by category and by circuit

Source: BIO / AND-I Agency – 2018

French Organic Market the majority of sales are “made in France”

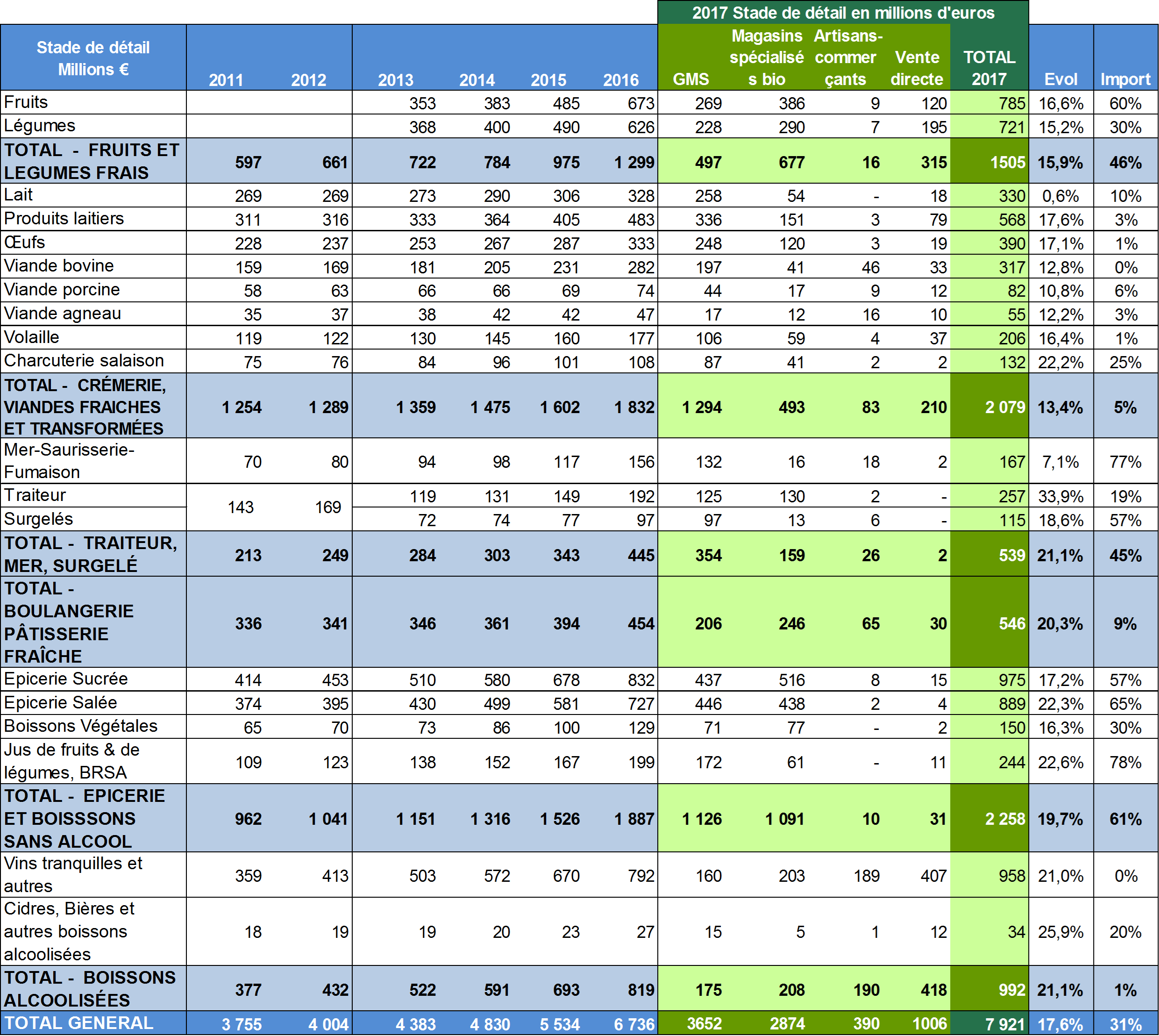

69% of organic products consumed in France are produced in France. 31% of organic products consumed in France were imported in 2017 versus 29% of products in 2016, + 2 points.

At the wholesale stage, the value of organic food imports increased by + 27%. However, more than 40% of the value of these imports can be considered as exotic (banana, cocoa, coffee …) or purely Mediterranean (olives, citrus fruits …), France does not produce these products, well very little or not at all. Thus excluding exotic products, the French supply of organic products is 82%.

Imports related to cyclical factors

Some products such as organic milk have been in short supply at the European level requiring imports, hence a slightly higher figure. On the territory, the poor growth of fodder in 2016 has led to a decline in organic milk production. The introduction of organic herds (converted in 2015) in 2017 and a more favorable climate led to an increase of 13.6% in the organic milk collection.

Necessary imports

French organic farmers can not produce everything. The development of sales of bananas and citrus weighs on the organic trade balance of France. These products, which are almost exclusively imported, alone account for one-third of organic fresh fruit and vegetable sales.

“Off-season” imports

Particularly used for organic fruits & vegetables, imports of “off-season” is to fill the shelves of products from the import to announce and thus launch the next arrival of seasonal products.

Supply chains that work with their French producers

Production from France is improving for several products such as field crops or onions. Many producer commitments allow their development accompanied by the contractualization with downstream operators. Thus, the share of onions “origin France” has increased from 43% of the value at the wholesale stage in 2014 to 64% in 2017. The development of French production has allowed to regain market share while accompanying the development of it.

Similarly, despite a very strong demand in 2017 and a disappointing harvest of organic potatoes at the end of 2016, due to a climate incident, the “origin France” potatoes rate remained in value, rising from 83% at 82%.

Half of the imported products come from European Union countries and half from the rest of the world.

43% of imports are made up of exotic products (banana, cocoa, coffee, etc.) or purely Mediterranean (olives, citrus fruits, etc.), with France producing no or very little of these products.

Origin of supplies according to organic products in 2017

Source: BIO Agency / AND-I 2018

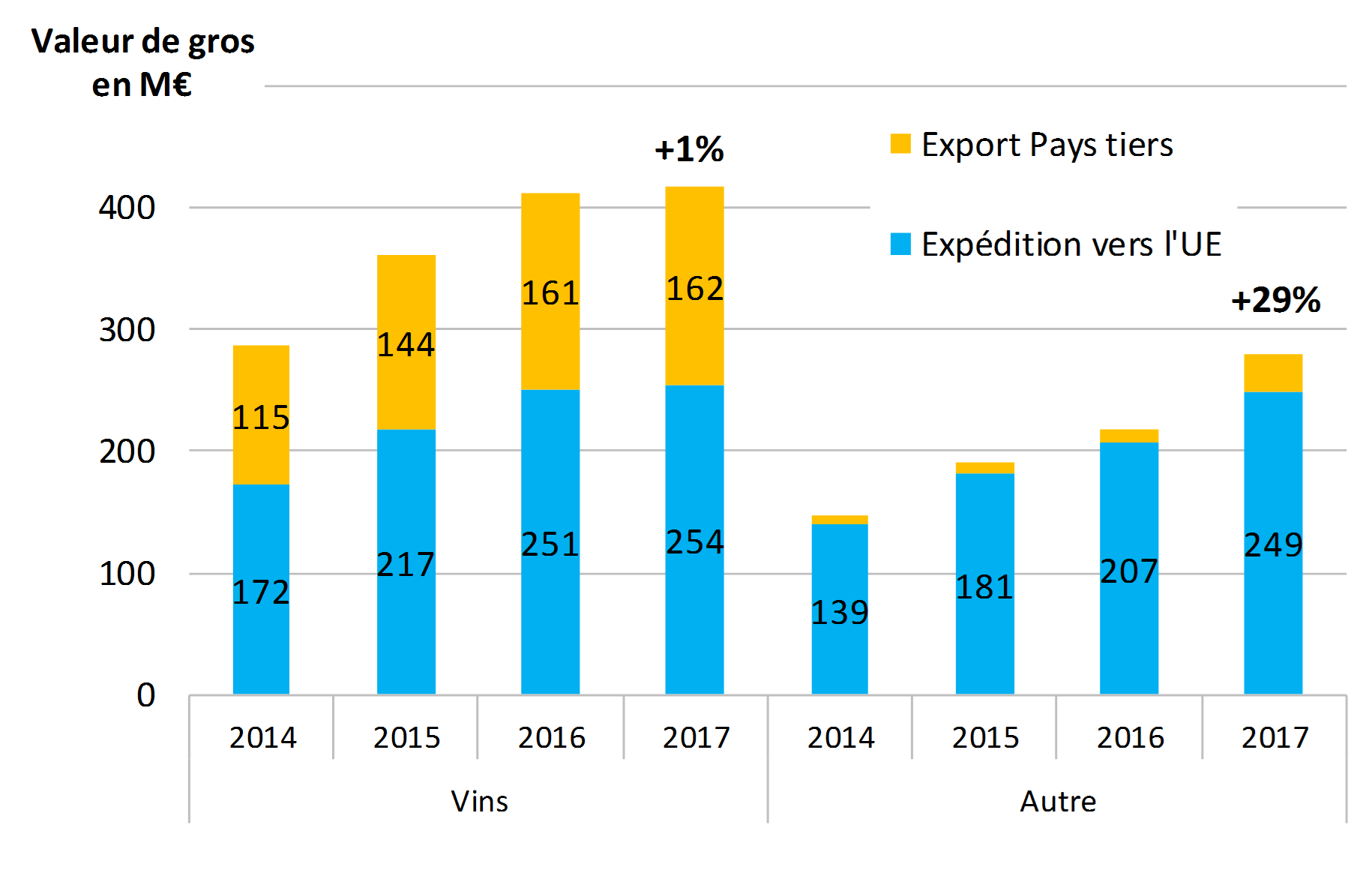

Exports of organic products: a growth of 12%

Despite significant domestic demand, French companies sold 707 million euros of organic products for export in 2017 (up + 12% from 2016).

Wines represent 59% of French exports of organic products in value but other sectors are developing in 2017 as the sweet and salty grocery (+ 59M €) and the sale of cider and organic beer: + 11M €.

Evolution of the value of exports of organic products between 2013 and 2017

Llnks to download the Agence Bio Reports on the French Organic Market

French Organic production data,

French Consumers of organic products.